The Australian government has announced a significant change to the Superannuation system, which will come into effect from 1st July 2026. The key change is that employers will be required to pay superannuation each payday rather than the current quarterly payment. This change, though still a few years away, is likely to present some challenges for Recruitment Agencies.

Paying employees their superannuation each payday is undoubtedly beneficial for them. By bringing forward their super payment, employees have the opportunity to accumulate more for their retirement, as the earlier access to funds allows for an increased return on investment. According to government estimates, employees can expect to be 1.5% better off at retirement on average. Additionally, this payment system makes it easier for employees to keep track of their super payments and reduces the likelihood of them being exploited by unscrupulous employers.

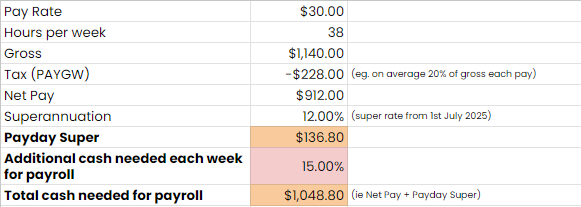

The Recruitment Industry is a major player in the Australian economy, with an estimated revenue of $16.4 billion in 2022, mostly derived from on-hire placements of temporary and contract employees with clients' businesses. As most agencies pay their employees weekly, managing cash flow is critical to sustaining the business. With the implementation of payday super, employers will need to allocate approximately 15% more funds to cover superannuation payments, compared to a standard pay week.

With over 25 years of experience in the Recruitment Industry, initially as agency owners and later as SaaS providers, we have witnessed two concerning trends: the erosion of margins and the extension of payment terms. Both of these developments have had a negative impact on the industry.

As the Recruitment Industry has expanded, competition among agencies has intensified, resulting in a decline in gross margin for on-hire placements. Furthermore, the industry has become more challenging with increased complexities and risks. While payday super is an excellent initiative, its implementation is expected to present additional difficulties for recruitment agencies. Thus, it is wise to take action now. Agencies must concentrate on improving their margins to sustain the increased cash requirements that payday super will necessitate.

To achieve this, agencies can start by shortening the length of payment terms offered to clients. Over the years, we have been astonished to see some agencies extending payment terms that are clearly unfeasible, such as 60, 90, or even 120+ days. In reality recruitment agencies, like any other employer, cannot delay paying their employees, including the upcoming payday super payments. Therefore, clients' expectations of an agency waiting for payment beyond seven days must be reevaluated.

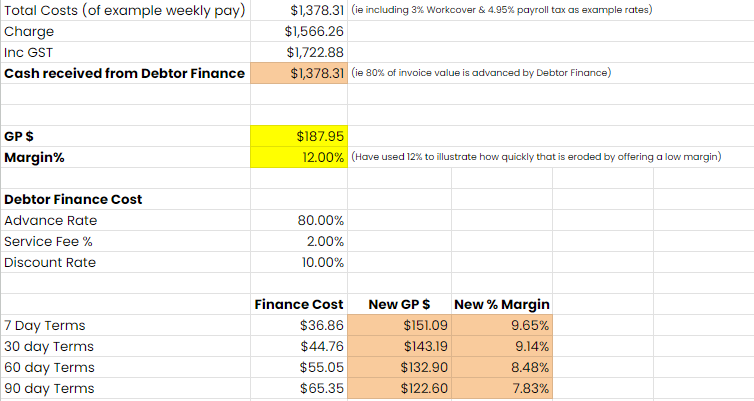

Especially in the current environment of increasing interest rates, it is crucial for agencies to improve their understanding (and communication) of the costs associated with extending payment terms, while also focusing intently on their margins. To demonstrate this, consider the scenario below, which examines the funding costs (and impact on margins) for an agency to finance a range of payment terms, using a non-bank debtor finance provider.

The above example vividly illustrates how an agency's margins can rapidly decline if it chooses to combine a low margin charge rate with extended payment terms. Furthermore, given the often significant credit risk that many agencies face with clients who are unable to pay (an issue we encountered firsthand during our agency ownership), agencies pursuing growth through low margins and extended payment terms are highly likely to struggle in the coming years. In short, such practices increase the risk of going out of business.

Seize the chance to proactively communicate with your clients today about why they choose your agency and the unparalleled advantages they reap from doing so. Simultaneously, leave no room for doubt that relying on your agency as an interest-free (non-recourse) source of funding for their payroll is not one of those benefits! The time to act is now, and a clear message to your clients can help ensure a sustainable future for your agency.

Founded in 2017, RecruitOnline combines 20+ years of recruitment expertise to deliver a tailored all-in-one platform built by recruiters for recruiters in Blue Collar and Healthcare. Integrating ATS, CRM, and multi-channel recruitment marketing, it streamlines hiring with seamless onboarding, intelligent workflows, built-in compliance, and AI-driven insights. Optional add-ons like the Candidate Mobile App, RecruitChatBot, and PinvoiceR further enhance efficiency by simplifying scheduling, automating tasks, and managing payroll and invoicing.